Iran Conflict and Dubai Real Estate: Sentiment Shock or Structural Risk?

The escalation of tensions involving Iran and parts of the Gulf has once again brought Dubai’s real estate market under the spotlight.

Summary

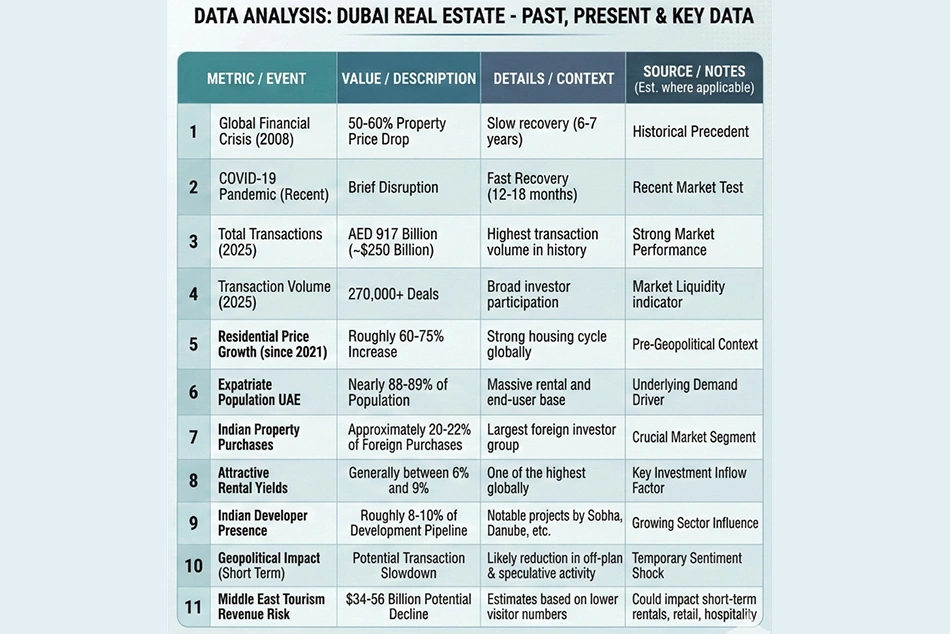

- In 2025, Dubai recorded AED 917 billion (~$250 billion) in real estate transactions, the highest in its history.

- Dubai offers some of the highest rental yields globally, generally ranging between 6% and 9%.

- Indian nationals are the largest foreign investor group, accounting for 20–22% of all foreign property purchases.

- Residential property prices in Dubai have surged by approximately 60–75% since 2021.

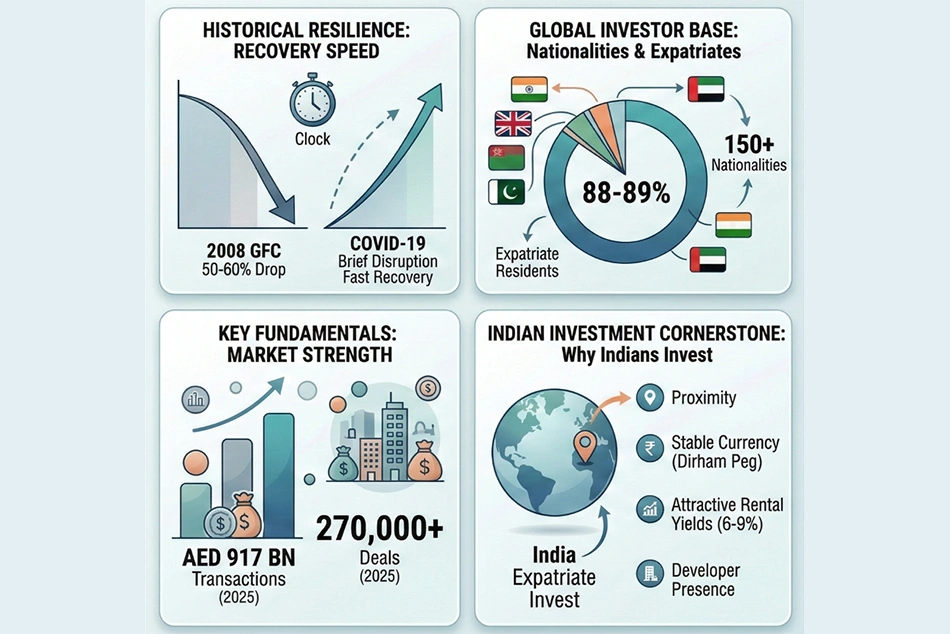

- 2008 crisis saw a 50–60% price drop, but market showed increased resilience during COVID-19, recovering in just 12–18 months

The escalation of tensions involving Iran and parts of the Gulf has once again brought Dubai’s real estate market under the spotlight. With reports of attacks reaching parts of the UAE, investors are inevitably asking whether regional instability could derail one of the world’s most dynamic property markets.

While geopolitical tensions can temporarily affect investor sentiment, Dubai’s real estate market has historically demonstrated a remarkable ability to absorb shocks and recover relatively quickly. Understanding the likely impact of the current conflict, therefore, requires looking at both market fundamentals and past cycles.

A Record-Breaking Foundation: The 2025 Momentum

Dubai entered this phase of geopolitical uncertainty from a position of considerable strength. In 2025 alone, the emirate recorded nearly AED 917 billion (about $250 billion) worth of real estate transactions, the highest in its history. Transaction volumes crossed 270,000 deals, reflecting strong investor participation and deep liquidity in the market. Residential real estate has been a major driver of this momentum.

Approximately 200,000 residential transactions valued at around AED 538 billion were recorded during the year. Since 2021, residential property prices in Dubai have risen by roughly 60–75%, making it one of the strongest housing cycles globally in the post-pandemic period.

Psychology of the Market: Managing Investor Perception

This context is important because markets already experiencing strong expansion tend to respond to geopolitical shocks differently. In most cases, the initial impact is a slowdown in transaction activity rather than an immediate correction in prices.

The latest conflict also introduces a new dimension: Dubai itself has come under attack, testing the emirate’s long-standing reputation as a safe economic hub in the Middle East. While the physical damage from these incidents has been limited, the psychological impact on global investors cannot be ignored.

The ‘Wait-and-Watch’ Shift: Sensitivity in Off-Plan Segments

Dubai’s real estate market depends heavily on international investors and expatriate residents. Any perception of rising geopolitical risk can lead investors to temporarily adopt a wait-and-watch approach.

Such sentiment shifts typically affect off-plan purchases and speculative investments first, as these segments tend to be more sensitive to market confidence.

Tourism Ripple Effect: Risks to Hospitality and Retail

Tourism represents another potential transmission channel. The broader Middle East tourism industry is estimated to be worth around $367 billion annually, and prolonged tensions could weigh on travel sentiment across the region.

Industry estimates suggest that geopolitical instability could result in 23–38 million fewer visitors, potentially translating into a $34–56 billion decline in tourism revenues.

If that scenario unfolds, the immediate impact would likely be felt in short-term rental apartments, hospitality assets and retail properties located in tourist-heavy districts. However, Dubai’s residential real estate demand is not driven by tourism alone. The city’s large expatriate population continues to provide a stable base of housing demand.

Structural Strength: A Global and Diversified Investor Base

One of Dubai’s greatest structural strengths is the diversity of its investor base. Buyers from over 150 nationalities participate in the emirate’s property market, making it one of the most internationalised real estate ecosystems globally.

Expatriates account for nearly 88–89% of the UAE’s population, naturally driving housing demand across multiple segments.

The Indian Connection: A Cornerstone of Market Stability

India plays a particularly significant role in this ecosystem. Indian nationals account for roughly 20–22% of foreign property purchases in Dubai, making them the largest investor group in the market.

Several factors explain this trend, including geographical proximity, the stability provided by the UAE dirham’s peg to the US dollar, and relatively attractive rental yields that typically range between 6% and 9%.

Developer Expansion: The Rise of Indian-Origin Players

Indian developers have also begun expanding their footprint in the emirate. While the sector continues to be dominated by local giants such as Emaar, DAMAC, Nakheel and Meraas, Indian-origin developers are estimated to account for roughly 8–10% of the development pipeline.

Companies such as Sobha Realty, which has developed the Sobha Hartland community spanning nearly 8 million sq ft, and Danube Properties, which has launched more than 20 residential projects, have established a visible presence in the market. Other developers, including Shapoorji Pallonji Real Estate and Casagrand, have also entered Dubai with premium developments.

History as a Guide: Navigating Two Decades of Cycles

Dubai’s real estate sector has experienced several cycles over the past two decades. During the 2008 global financial crisis, property prices declined by nearly 50–60%, and the market took roughly 6–7 years to fully recover. A second correction occurred between 2014 and 2019, when prices fell by around 25–30%, driven largely by lower oil prices and oversupply.

More recently, the COVID-19 pandemic caused only a brief disruption, with the market recovering within 12–18 months. These cycles highlight an important feature of Dubai’s property market: while corrections can be sharp, the sector has historically demonstrated a strong capacity to recover once investor confidence stabilises.

The Verdict: Short-Term Caution vs. Long-Term Potential

The current geopolitical tensions will undoubtedly introduce a degree of caution among investors. Transaction volumes may moderate in the near term as buyers assess the evolving risk environment. Yet Dubai’s position as a global financial and lifestyle hub, combined with its diversified investor base and policy flexibility, continues to provide strong structural support to its real estate sector.

In that sense, the real question may not be whether geopolitical tensions will affect Dubai’s property market - they almost certainly will in the short term. The more relevant question is how quickly investor confidence returns once the geopolitical environment stabilises. If history is any guide, Dubai’s real estate market has repeatedly demonstrated that it can recover faster than many global property markets.

[The writer, Dr. Prashant Thakur, is Executive Director & Head - Research & Advisory, ANAROCK Group, Pune.]

Follow ummid.com WhatsApp Channel for all the latest updates.

Select Language to Translate in Urdu, Hindi, Marathi or Arabic